MONEY

The money monk

Becoming aware of my money type helped me to loosen up and enjoy life more.

“No one can be the slave of two masters: he will either hate the first and love the second, or treat the first with respect and the second with scorn. You cannot serve both God and money.” (Matthew 6:24)

I grew up in a religious family. We were weekly churchgoers and observed the year’s festivals very much from a spiritual rather than materialistic perspective. It was also an academic family and strongly valued the spiritual and intellectual over the materialistic. It was certainly not a cold or austere upbringing. But everything that I learned and observed from my parents reinforced a money belief that ‘you can’t serve two masters’.

The characteristics of a money monk

As a consequence, a large part of my money type is what Maggie Baker, in her book Crazy About Money, refers to as the ‘money monk’:

“Essentially, money monks believe that there is something immoral about liking money, that the love of money is the root of all evil and that it will be a corrupting influence. A money monk’s self-esteem comes from the satisfaction of feeling superior to money and those who seek it. Their sense of self is centred in the essential values in life. They don’t want to be dirtied by glossy, earthly pleasures or corrupted away from a sense of value.”

Kind of ironic then that I ended up consulting in executive pay and working as a financial coach. But that’s for another blog. Who says we have to be consistent?

This may be overstating my money beliefs a bit, but there’s been an uncomfortably strong element of truth in this description.

Neither good nor bad

As with most money beliefs it’s neither all good nor all bad. There are positive and negative implications.

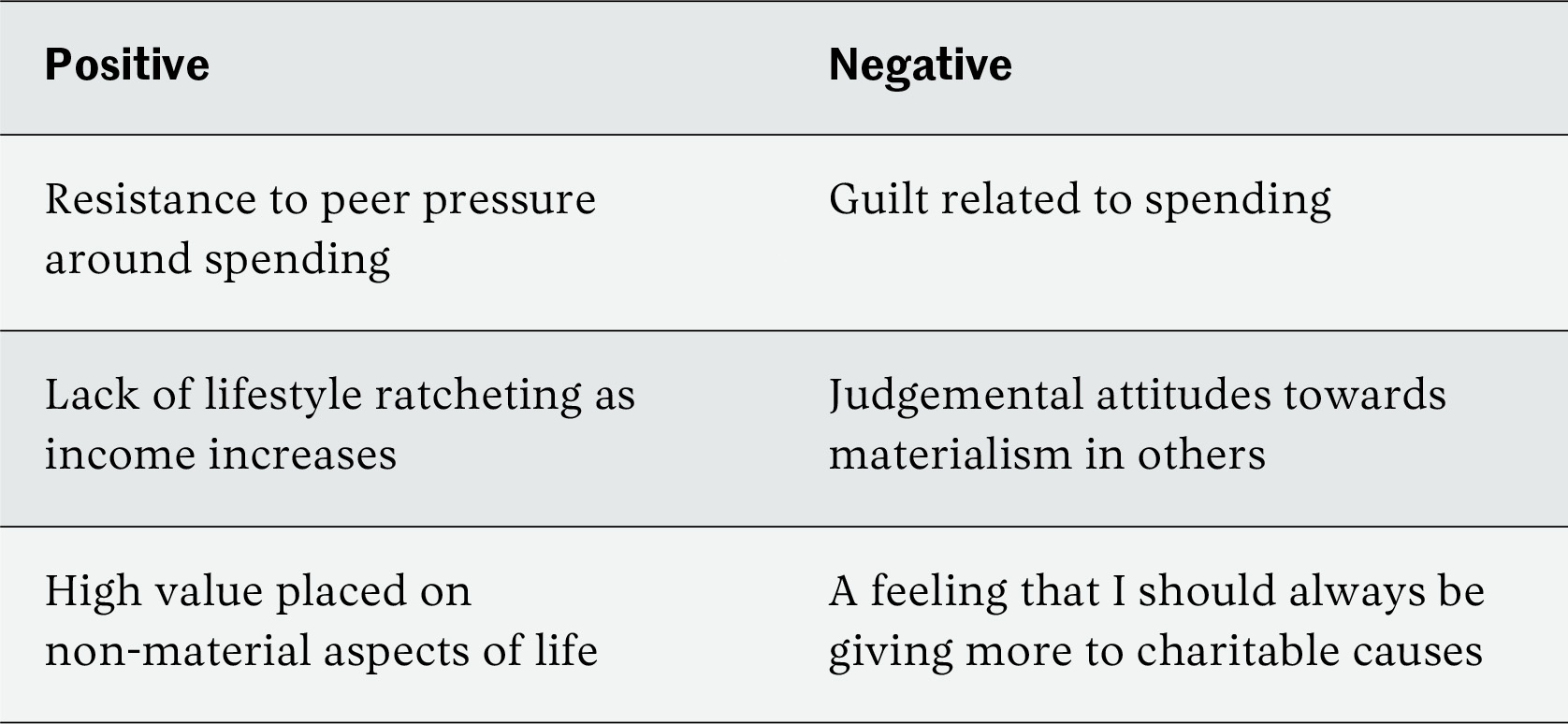

This money belief had some positive aspects. The imperviousness to peer pressure and lifestyle ratcheting enabled us to build a surplus of income over expenditure for investment. The value I place on non-material aspects of life enabled me to trade money for time as I went progressively more part-time through my career — by itself that has enabled me to live a richer life. Supporting charitable causes is a good thing.

But there are negative dimensions to this money belief, in particular the overhang of guilt around spending and charitable giving. Anything is bad, taken to extremes. Indeed, at one point I flirted with the idea that as I was in a high-earning career, I had a duty, once I had enough money for financial independence, to work as long as possible and give everything I earned to charity.

Clearly these attitudes would prevent me and my family from enjoying the life we now have. Indeed, excessive guilt about spending money undermines financial freedom in the psychological sense as much as excessive attachment to money.

I could also be a bit of a pain in the backside with my family, going grumpy if I felt my children were showing too much of a materialistic attitude towards shopping trips (it wouldn’t have crossed my parents’ minds that shopping could be a leisure pursuit) or holiday destinations (amazingly, holidays in Northumberland or South Wales aren’t enough for some people every year). In fact, in the wrong mood, I could be as tight as a [insert your favourite metaphor].

Reframing beliefs

Understanding your money beliefs and where they come from is the first step to enabling change. The mere act of naming what’s going on creates perspective. You can work on reframing those beliefs in a more positive way in light of your higher motivations and goals. And it’s then possible to design simple actions that enable you to experience the change you want to become.

In the money factor I work with clients on reframing money beliefs that are no longer serving them. In my own case, I reframed ‘You can’t serve two masters’ into a pair of related money beliefs: ‘I can spend money without serving money’ and ‘I don’t have to be perfect to be good.’

It’s not quite as simple as telling yourself to have a different belief. But we can choose how to think about things more than we think, and the perspective gained by reframing is the first step in loosening old emotional ties.

The next step is to take actions that help to reinforce the belief through experienced behaviour. A simple behaviour change was to accept that shopping trips are a legitimate part of someone else’s holiday, to be prepared for the feelings that would be triggered in me, but to focus on the companionship of the trip and to be prepared to work through the discomfort. A shopping trip would also include a social family meal or drink (which I value highly) and that was likely to be much more positive if the kids had done something they enjoyed as opposed to being dragged around a tired, old monument.

Rules, routines and changes to your environment that support change can also be very helpful. To overcome guilt about spending we’ve made a conscious decision about how much to give to charity each year, how much to save and how much to spend. Using my reframed money belief I was able to make peace with my compromise. Setting up a conscious allocation for how we use our money takes endless second guessing off the table.

I don’t want to present this as being a magic wand that waves away all problems. But in the money factor I go through a process that really does make a difference. Of creating awareness about the issue, accessing motivation to change, acting the change and reflecting on and rewarding changed behaviour.

Money types are well ingrained but not immutable. But if they’re not acknowledged they can never be changed.